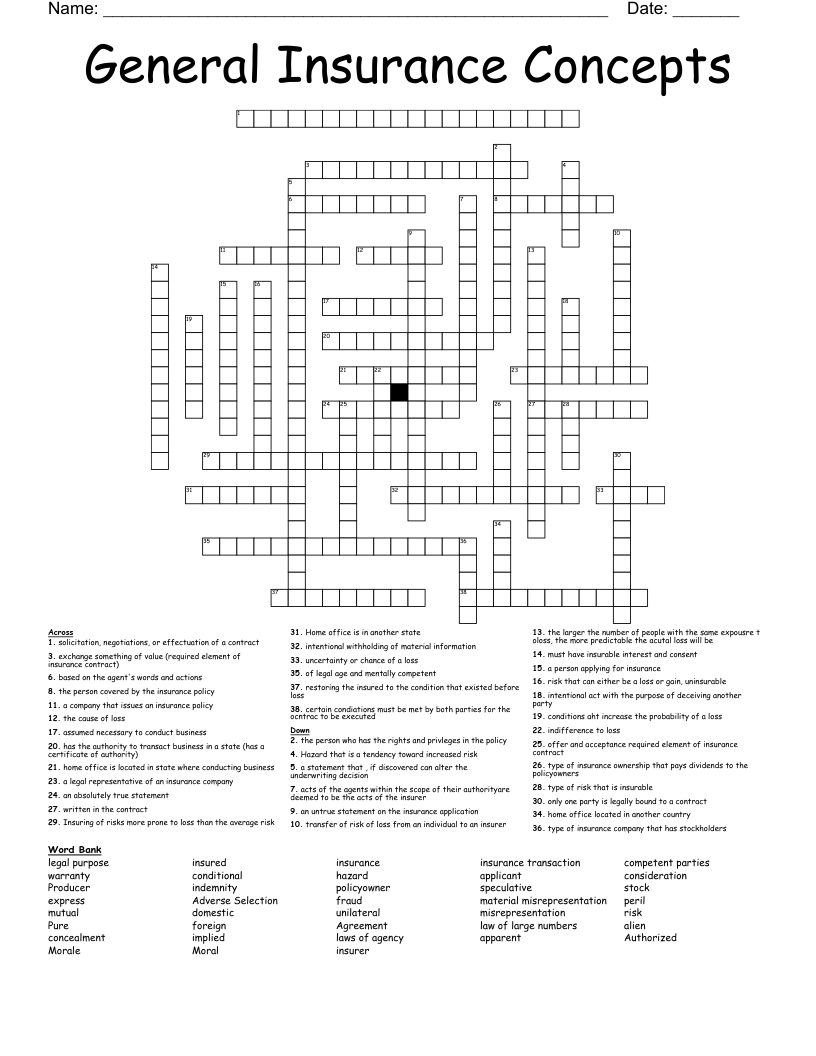

General Insurance Crossword

This printable crossword puzzle on the topic of Economics & Business has 24 clues. Answers range from 4 to 25 letters long. This crossword is also available to download as a Microsoft Word document or a PDF.

Description

Is the uncertainty or chance of a loss occurring

Refers to situations that can only result in a loss or no change. There is no opportunity for financial gain. Is the only type of risk that insurance companies are willing to accept

Involves the opportunity for either loss or gain. An example is gambling. These types of risks are not insurable.

Are conditions or situations that increase the probability of an insured loss occurring. classified as physical or moral

Are the causes of loss insured against in an insurance policy.

Is defined as the reduction, decrease, or disappearance of value of the person or property insured in a policy, caused by a named peril. Insurance provides a means to transfer...

Elimination of exposure to a loss

Is the planned assumption of risk by an insured through the use of deductibles, co-payments, or self-insurance

Is a method of dealing with risk for a group of individual persons or businesses with the same or similar exposure to loss to share the losses that occur within that group.

Moving risk from an individual or group to an insurace company.

A loss that is outside the insured’s control.

A loss that is specific as to the cause, time, place and amount. An insurer must be able to determine how much the benefit will be and when it becomes payable.

Insurers must be able to estimate the average frequency and severity of future losses and set appropriate premium rates. (In life and health insurance, the use of mortality tables and morbidity tables allows the insurer to project losses based on statistics.)

Insurers need to be reasonably certain their losses will not exceed specific limits. That is why insurance policies usually exclude coverage for loss caused by war or nuclear events: There is no statistical data that allows for the development of rates that would be necessary to cover losses from events of this nature.

There must be a sufficiently large pool of the insured that represents a random selection of risks in terms of age, gender, occupation, health and economic status, and geographic location.

Insurance companies strive to protect themselves from; the insuring of risks that are more prone to losses than the average risk. Poorer risks tend to seek insurance or file claims to a greater extent than better risk

States that the larger the number of people with a similar exposure to loss, the more predictable actual losses will be

Is authority that is not expressed or written into the contract, but which the agent is assumed to have in order to transact the business of insurance for the principal. Is incidental to and derives from express authority since not every single detail of an agent’s authority can be spelled out in the written contract.

Is the authority a principal intends to grant to an agent by means of the agent’s contract. It is the authority that is written in the contract.

Is the appearance or the assumption of authority based on the actions, words, or deeds of the principal or because of circumstances the principal created. For example, if an agent uses insurer's stationery when soliciting coverage, an applicant may believe that the agent is authorized to transact insurance on behalf of the insurer.

Is something of value that each party gives to the other.

There is an exchange of unequal amounts or values

Untrue statements on the application are considered and could void the contract.

Is a statement that, if discovered, would alter the underwriting decision of the insurance company