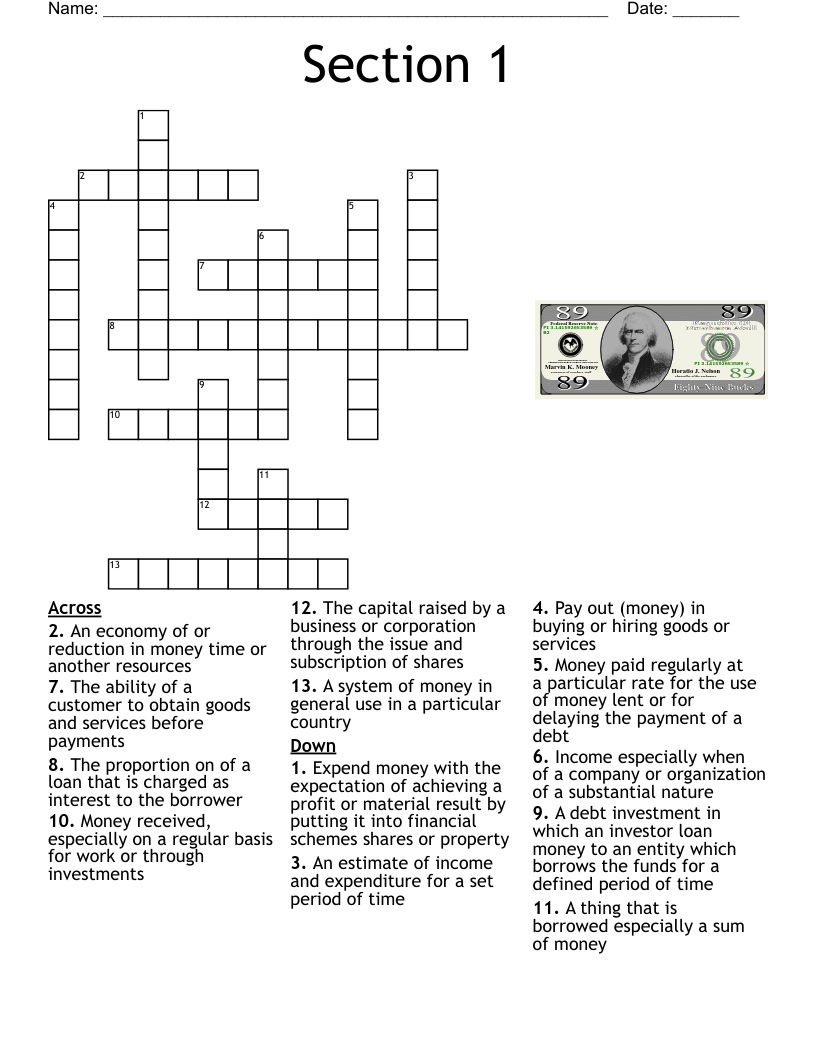

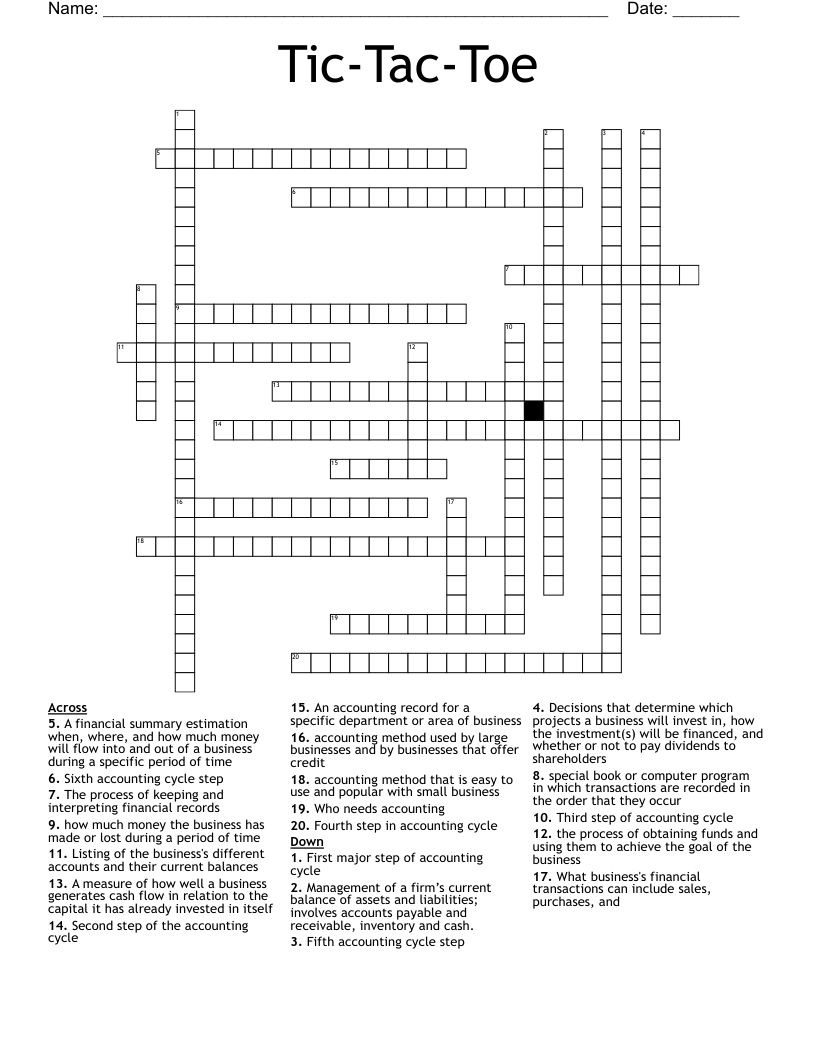

Tic-Tac-Toe Crossword

This printable crossword puzzle on the topic of Economics & Business has 20 clues. Answers range from 6 to 30 letters long. This crossword is also available to download as a Microsoft Word document or a PDF.

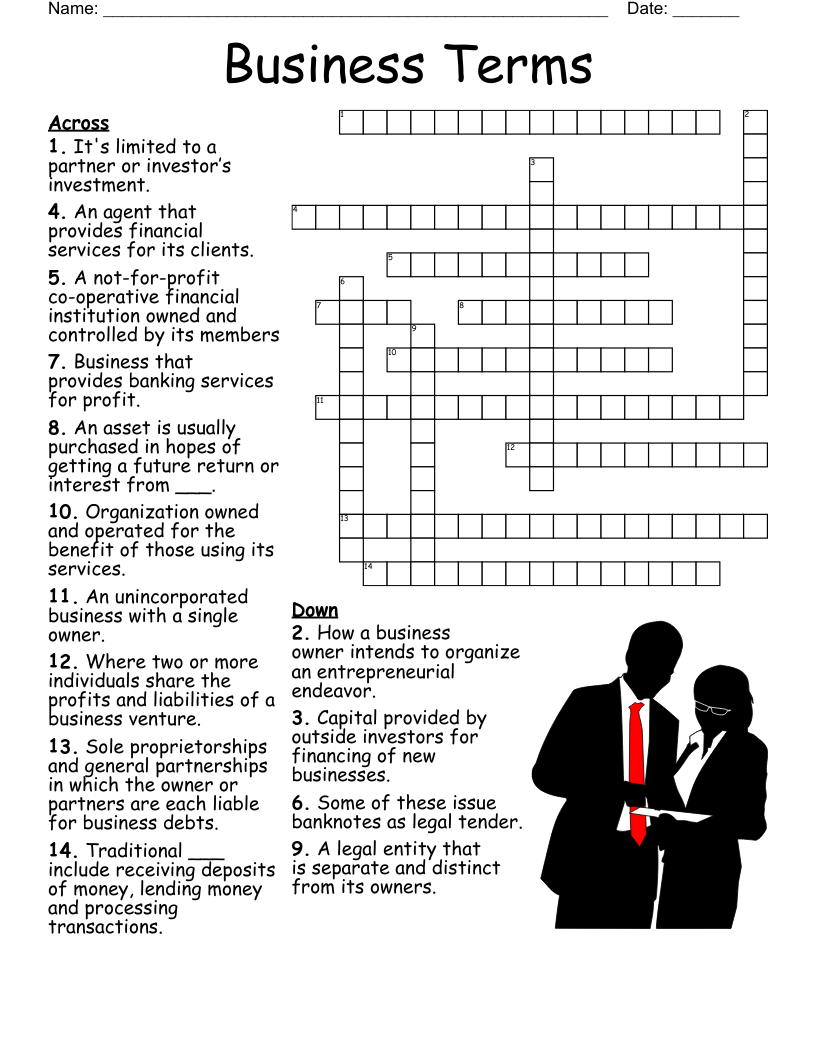

Description

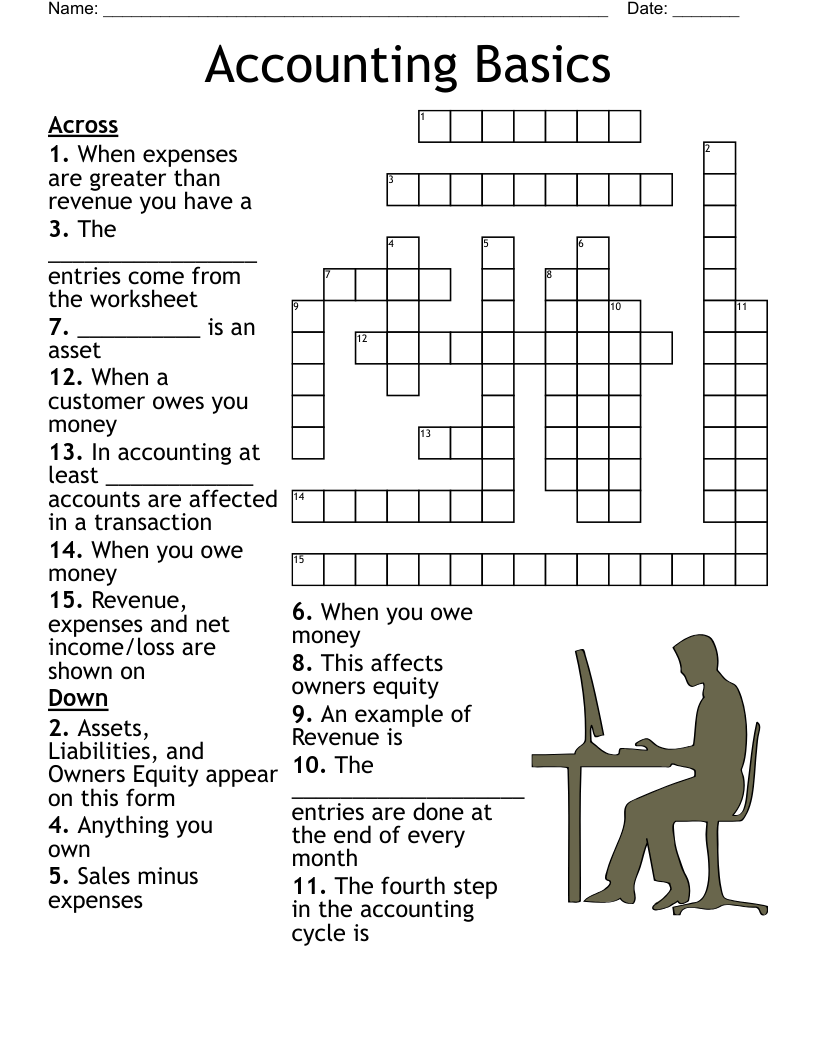

The process of keeping and interpreting financial records

the process of obtaining funds and using them to achieve the goal of the business

Decisions that determine which projects a business will invest in, how the investment(s) will be financed, and whether or not to pay dividends to shareholders

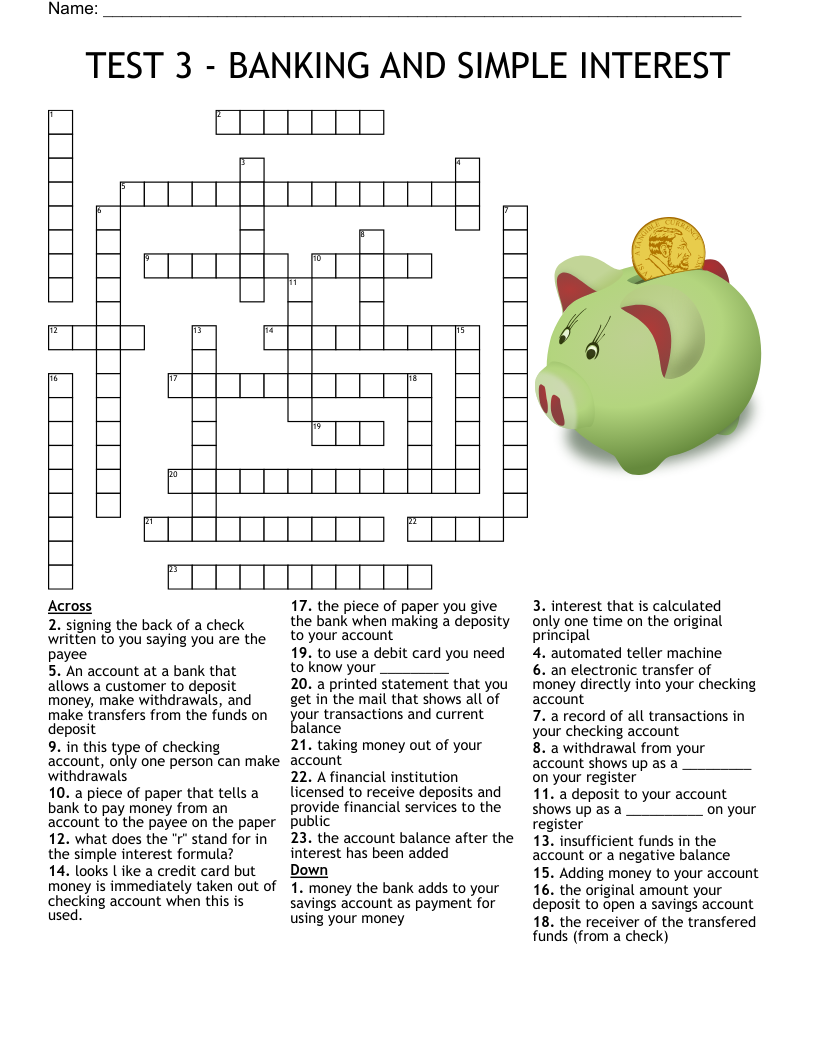

Management of a firm’s current balance of assets and liabilities; involves accounts payable and receivable, inventory and cash.

A measure of how well a business generates cash flow in relation to the capital it has already invested in itself

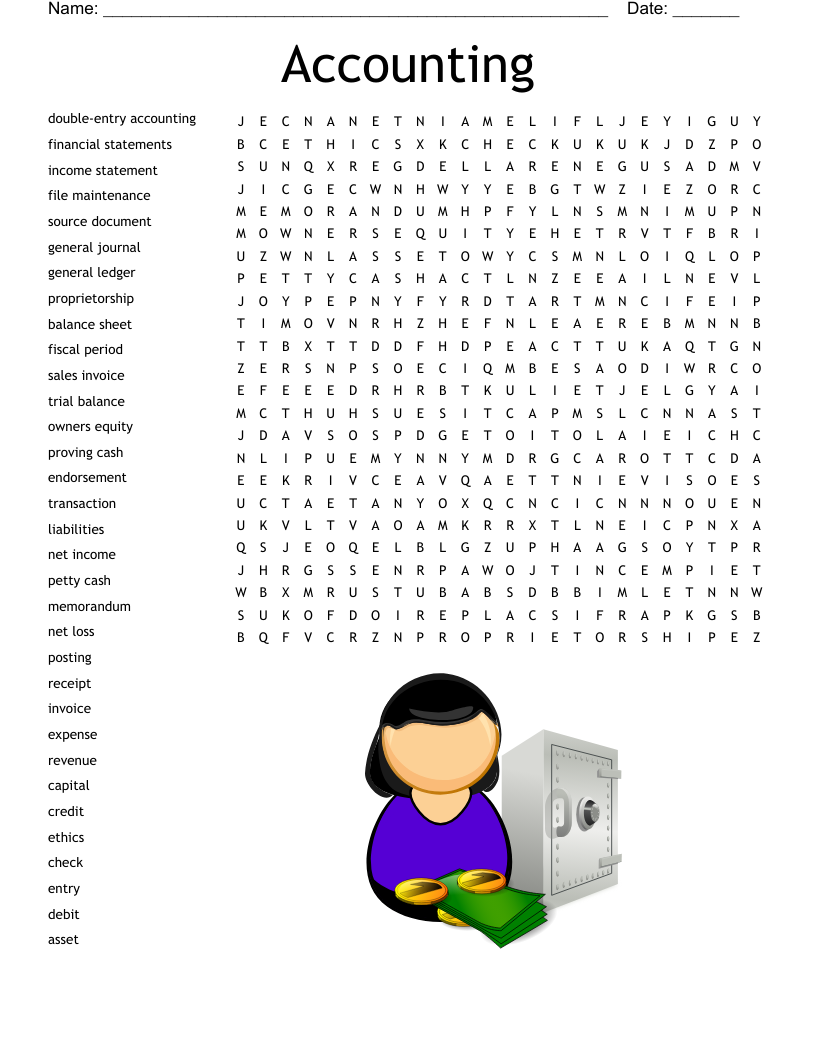

special book or computer program in which transactions are recorded in the order that they occur

accounting method that is easy to use and popular with small business

accounting method used by large businesses and by businesses that offer credit

An accounting record for a specific department or area of business

Listing of the business's different accounts and their current balances

how much money the business has made or lost during a period of time

A financial summary estimation when, where, and how much money will flow into and out of a business during a specific period of time

Who needs accounting

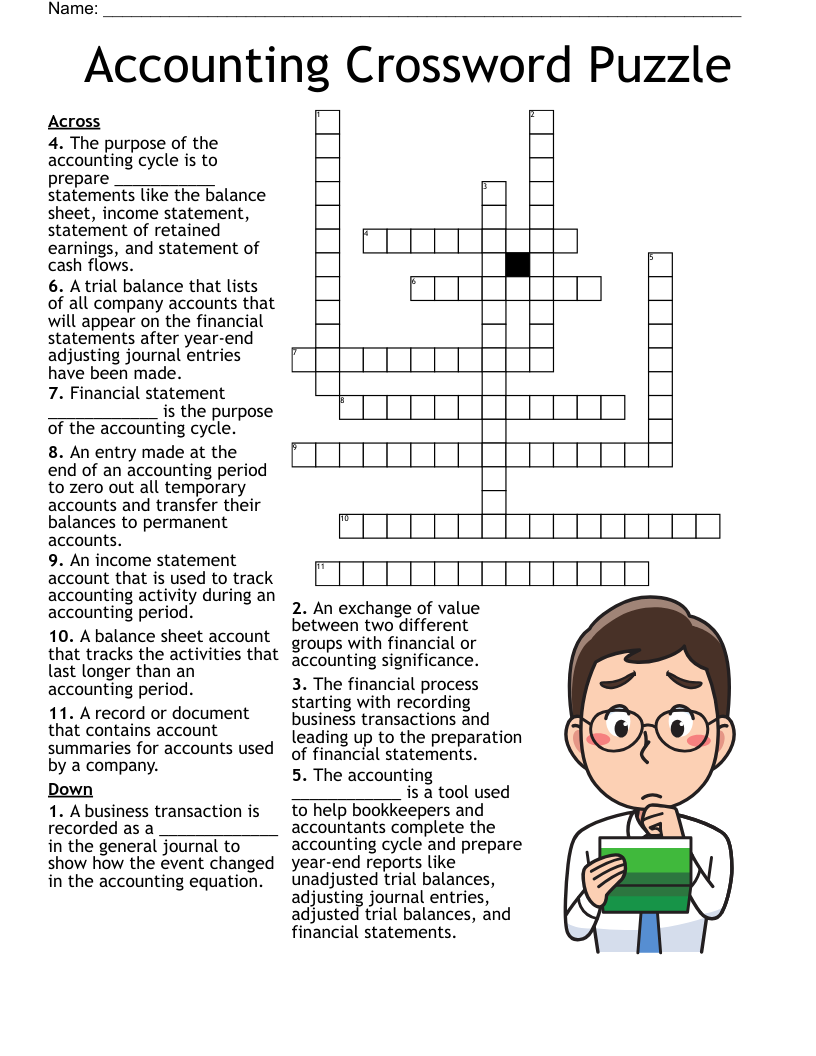

First major step of accounting cycle

Second step of the accounting cycle

Third step of accounting cycle

Fourth step in accounting cycle

Fifth accounting cycle step

Sixth accounting cycle step

What business's financial transactions can include sales, purchases, and