Marketing Unit 2 Vocab Quiz Worksheet

This printable matching worksheet on the topic of Economics & Business has 24 questions and answers to match. This matching worksheet is also available to download as a Microsoft Word document or a PDF.

Description

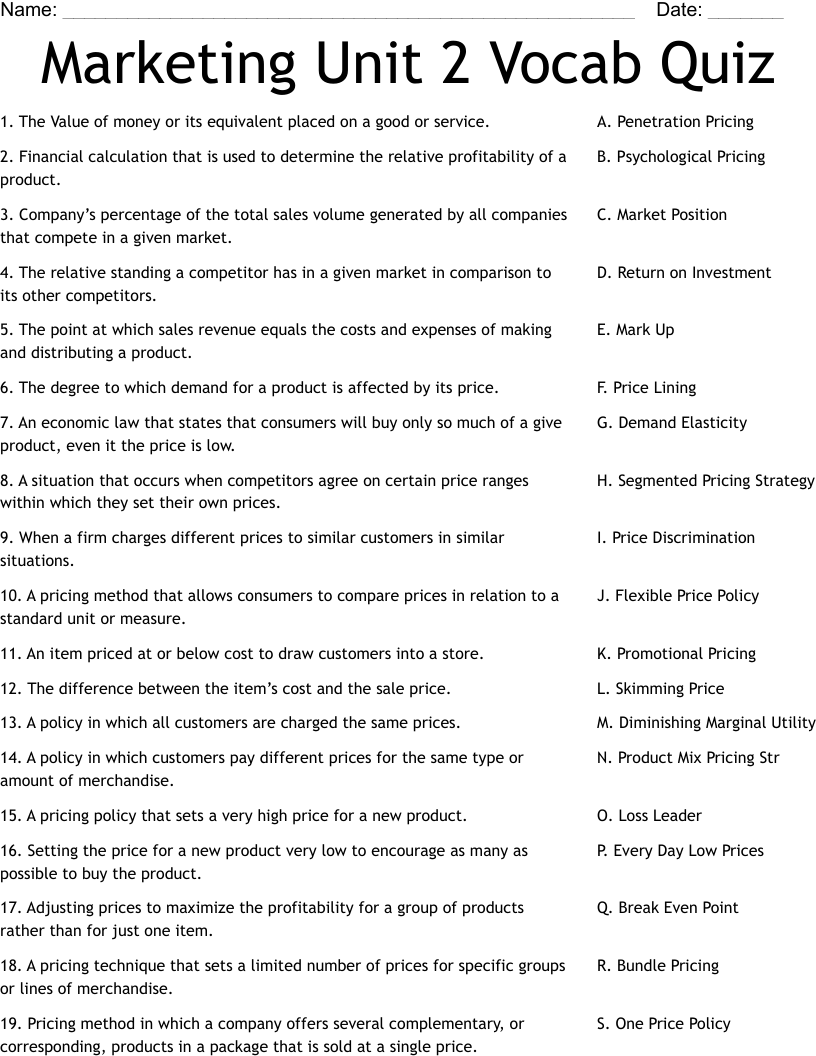

The Value of money or its equivalent placed on a good or service.

Financial calculation that is used to determine the relative profitability of a product.

Company’s percentage of the total sales volume generated by all companies that compete in a given market.

The relative standing a competitor has in a given market in comparison to its other competitors.

The point at which sales revenue equals the costs and expenses of making and distributing a product.

The degree to which demand for a product is affected by its price.

An economic law that states that consumers will buy only so much of a give product, even it the price is low.

A situation that occurs when competitors agree on certain price ranges within which they set their own prices.

When a firm charges different prices to similar customers in similar situations.

A pricing method that allows consumers to compare prices in relation to a standard unit or measure.

An item priced at or below cost to draw customers into a store.

The difference between the item’s cost and the sale price.

A policy in which all customers are charged the same prices.

A policy in which customers pay different prices for the same type or amount of merchandise.

A pricing policy that sets a very high price for a new product.

Setting the price for a new product very low to encourage as many as possible to buy the product.

Adjusting prices to maximize the profitability for a group of products rather than for just one item.

A pricing technique that sets a limited number of prices for specific groups or lines of merchandise.

Pricing method in which a company offers several complementary, or corresponding, products in a package that is sold at a single price.

Price adjustments required because of different shipping agreements.

A strategy that uses two or more different prices for a product, though there is no difference in the item’s cost.

Pricing techniques that create an illusion for customers.

Low prices set on a consistent basis with no intentions of raising them or offering discounts in the future.

Used in conjunction with sales promotions when prices are reduced for a short period of time.